February 6

Talking COVID, Russia, and climate

Hi all,

This week’s (well, technically last week’s) Energy Charts are posted at https://aleach.ca/charts.

We have stories this week from Marc and Yousaff. Marc is looking at the recent news stories on the potential for [orphaned renewable energy infrastructure](https://www.cbc.ca/news/canada/calgary/alberta-vulcan-county-orphan-wells-jason-schneider-1.6730467) to affect rural lands in the future, just as orphaned oil wells are causing issues today. As Marc points out, there is no split title issue for renewable energy so, if a wind or solar farm is using private land, it’s doing so under an agreement with the landowner just as would be the case for any other private business use of land. And, landowners are free to refuse wind or solar development and/or to impose any conditions they choose on the development. Might there be companies that default on their obligations? Sure. But, that’s not unique to renewable power.

Yousaff has a story on large clean energy investments in India - more than $4 billion dollars. As China and now India move ever faster on clean energy, their sheer scale will lead to spillovers and technological improvements that will benefit the global energy economy far beyond their borders.

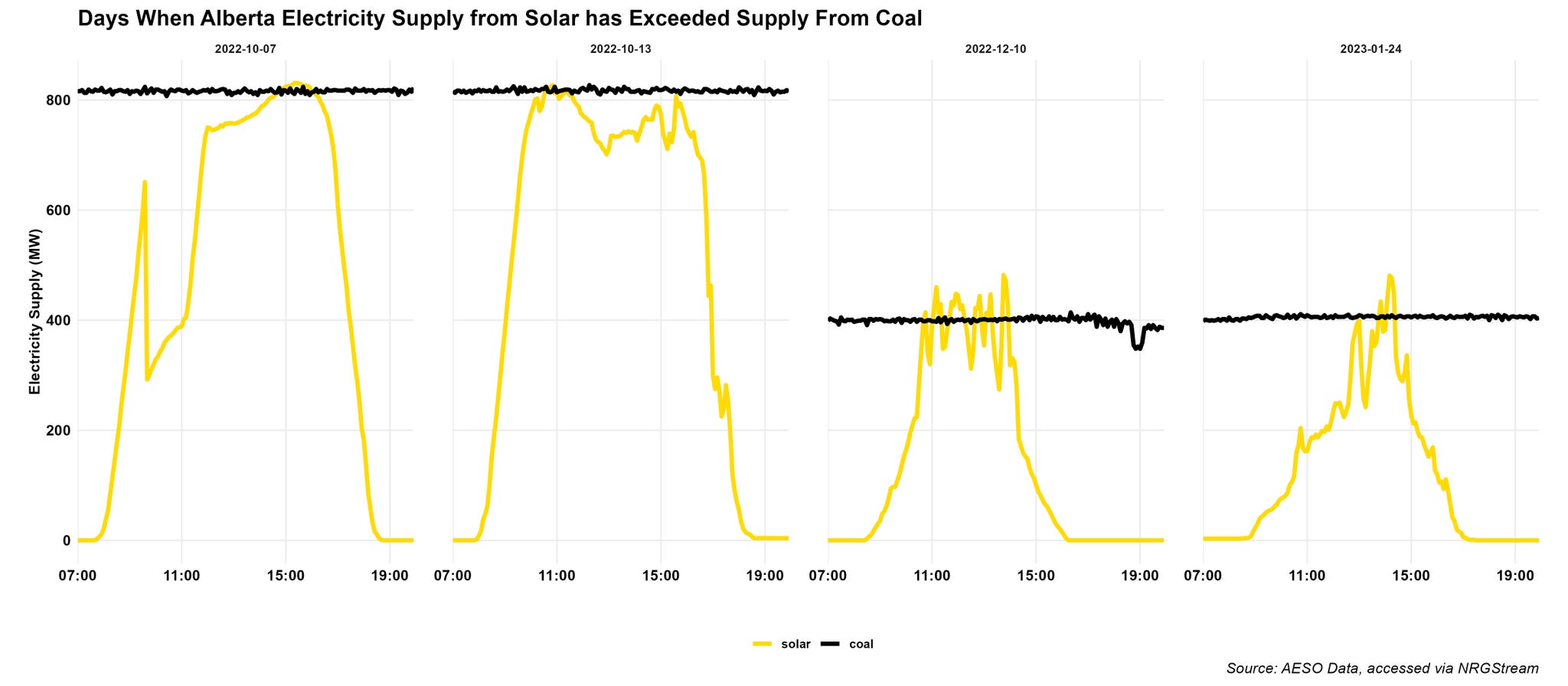

Also, a quick update on last week’s mailer: it turns out that there have been 4 days where solar generation has exceeded coal generation in Alberta since last fall.

Other than that correction, I’m using this mailer to get ready for a talk.

Tonight, along with Kathryn Harrison from the UBC, I am speaking at an event at the University of Alberta for our International Week with a focus on climate policy and recent disruptions in global energy markets.

The presentation ties-in to a paper that Professor Harrison and I have been working on (for too long already) that started as a COVID paper and has evolved to include changes in the climate policy environment in Canada after the Russian invasion of Ukraine.

The paper looks at how the Canadian climate policy environment has evolved since the 2015-16 oil price crash, through the downturn which followed, through COVID, and most recently through the turmoil in global oil and gas markets caused by Russia’s invasion of the Ukraine.

First, some background on climate change and Canada’s policy challenge.

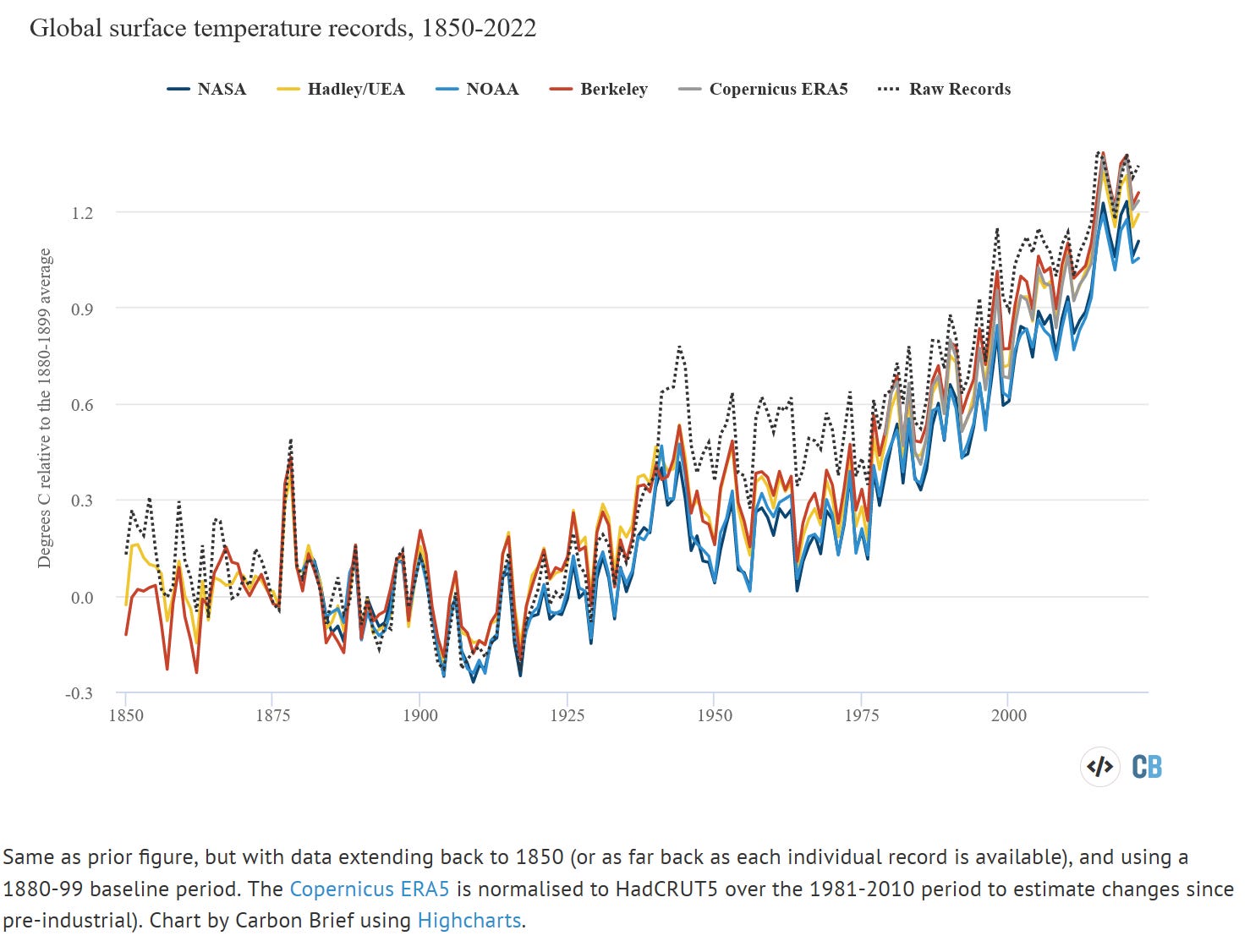

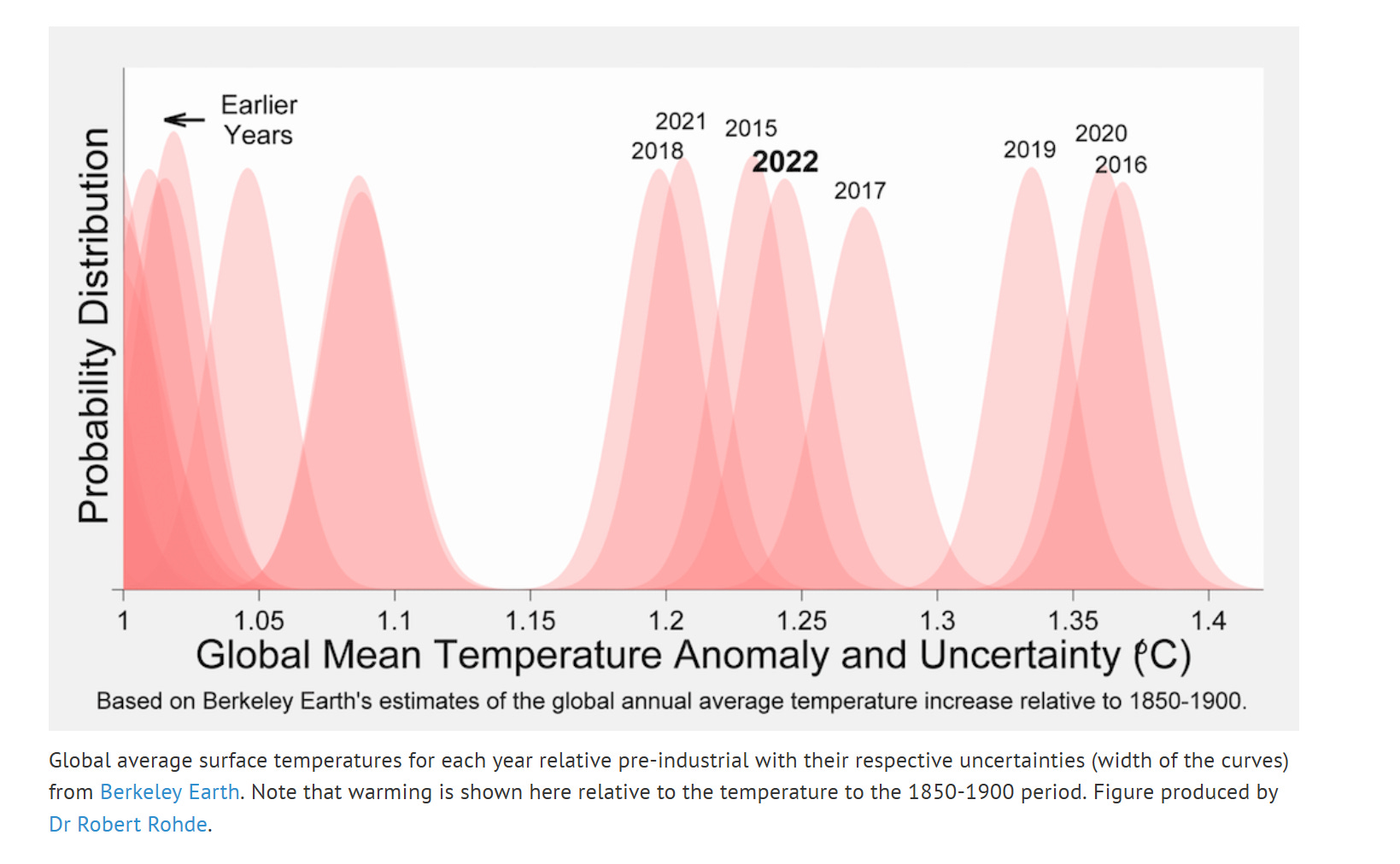

Zeke Hausfather’s annual climate change update came out at CarbonBrief last week, and using Zeke’s always great data visualizations, we can see that the global climate change picture continues to worsen. According to NASA, 2022 was the fifth warmest year on record, and all of the warmer years on record have occurred in the last decade. As usual, there are voices saying “the temperature hasn’t risen on average in the last X years”, which has been true for a number of X-year periods over the past 50 years. But, when you consider the complete time series, the picture is compelling, and more and more worrisome each year.

The picture gets more worrisome if you look at longer-term data.

And, yes, these points are measured with significant error. That doesn’t make things a whole lot better.

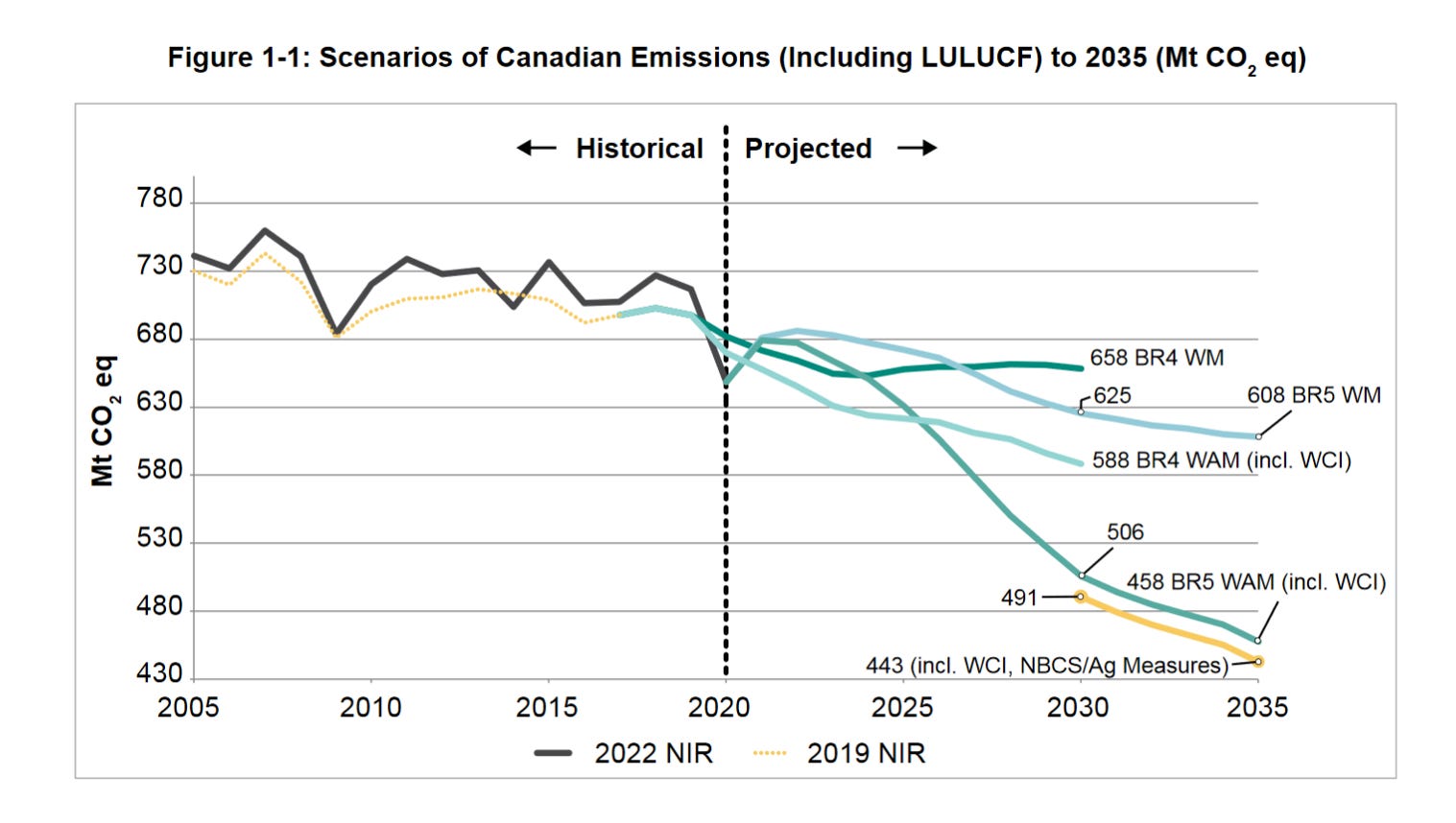

From a Canadian perspective, we’ve recently seen the release of Canada’s 5th Biennial Report to the United Nations on Climate Change, and the picture is not great here either.

Canada’s emissions continue to trend downward, and the new report contains at least one model run that shows Canada barely meeting its Glasgow target to see emissions 40-45% below 2005 levels by 2030.

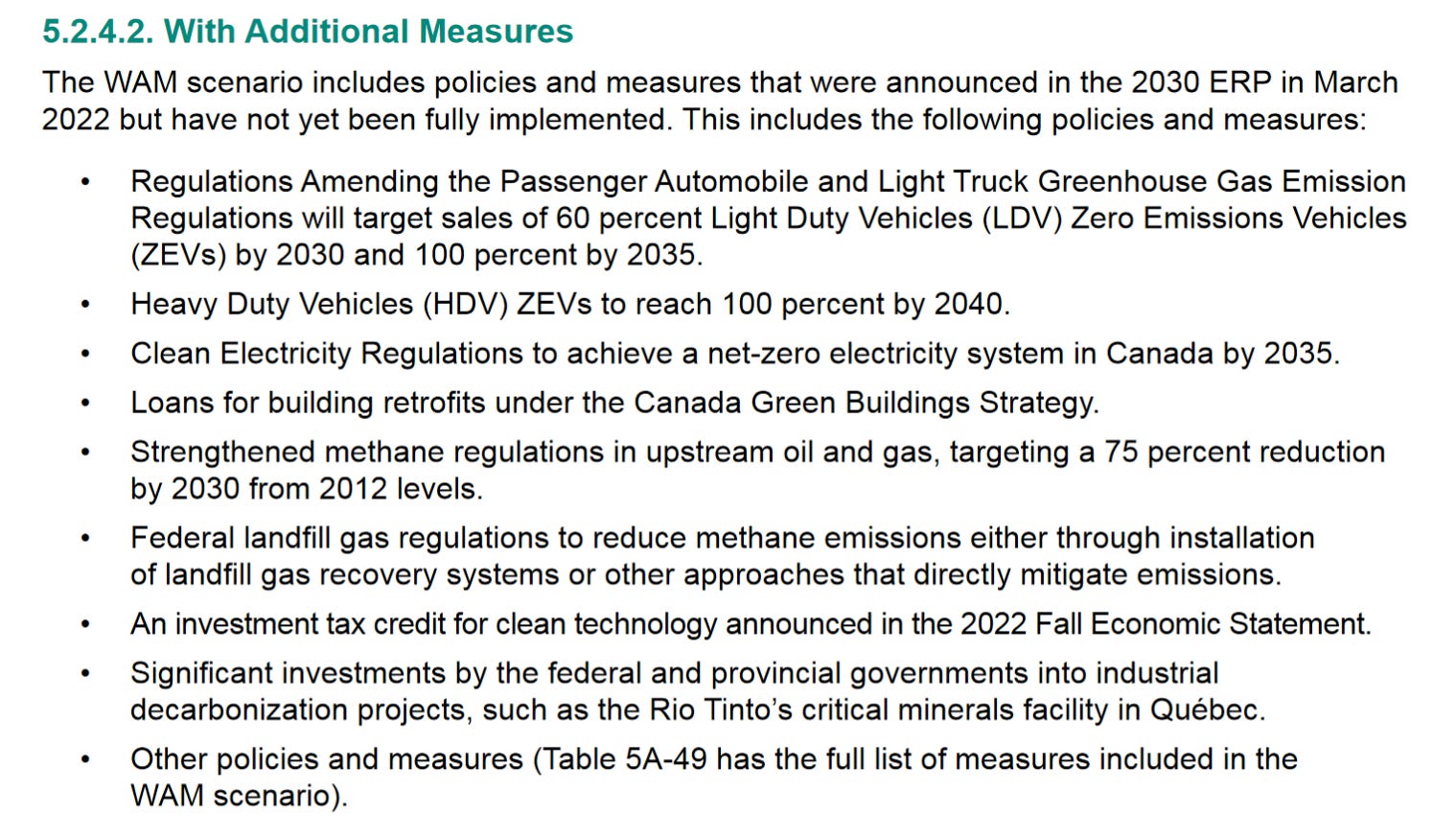

But, there’s an important story buried in the acronyms in the Figure below.

The 5th biennial report (BR5) with measures (WM) line, in light blue, is where our emissions are projected to be if we continue with all the measures currently implemented: the carbon pricing regime, the clean fuels regulation, etc. On that trajectory, our emissions end up at 608 Mt by 2035, 18% below our 2005 levels.

The with-additional-measures (WAM) line which gets Canada to 443 Mt (40% below 2005 levels) by 2030 is good news, but involves a lot of additional heavy lifting from new and existing policies.

What exactly? The BR5 report tells you:

And that’s just the beginning. Table 5A-49 has two pages of new policies, measures, and spending commitments from Ottawa, along with measures from some of the provinces (curiously, nothing is included for Alberta) on pages 317-318 of the BR5 report.

Back to what we’re talking about tonight: three things which have disrupted and will continue to disrupt Canadian action on climate change.

First, the oil price crash from 2015 through 2020:

And the crash in global investment in oil and gas that came with it.

These events meant that Alberta was feeling the pain of job loss and disruption long before many people had heard of the words just transition. This drop was global, as shown above, but it coincided with the imposition of carbon pricing in Alberta under the NDP and the election of Justin Trudeau federally. And, as with the justinflation canard, correlation is as good as causation in politics.

These changes damaged the momentum for carbon policy in Canada, and aided the rise of the resistance - the climate contrarian premiers in Alberta, Saskatchewan, Ontario and other provinces.

The biggest L for the resistance surely came when Justin Trudeau’s Greenhouse Gas Pollution Pricing Act was upheld by the Supreme Court in 2021, but that was overshadowed by what had happened in the year previous: the COVID-19 pandemic had ravaged the world and turned out country and most others upside down.

In oil markets, COVID led to a correction of massive proportions which took the wind out of the sails of the jobs, economy, pipelines promises of Alberta’s government and transformed Jason Kenney into an industrial-policy conservative, if there is such a thing.

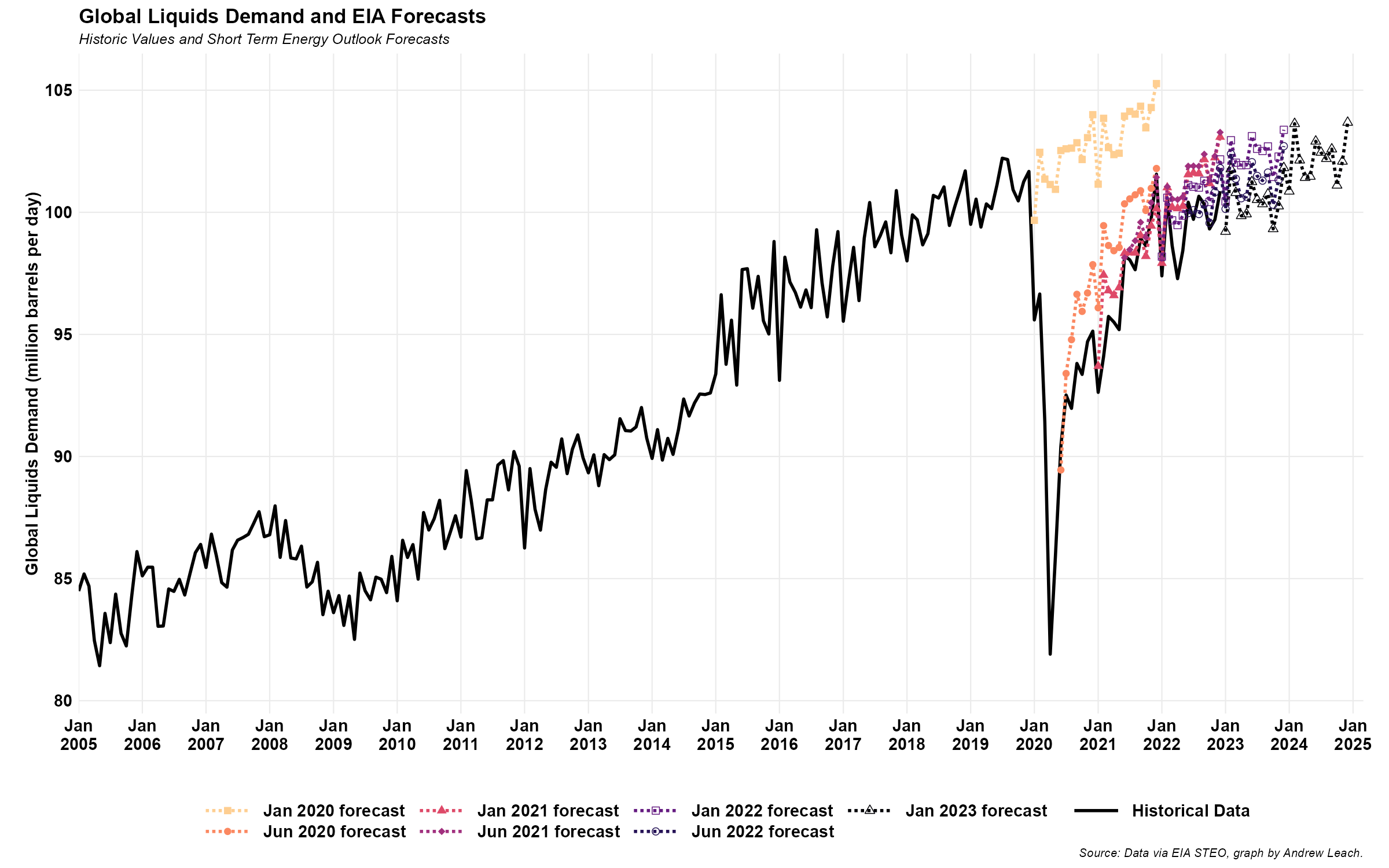

For tonight, though, I am focused on the correction in the oil markets that followed the pandemic declaration, and from which we have not yet seen a recovery.

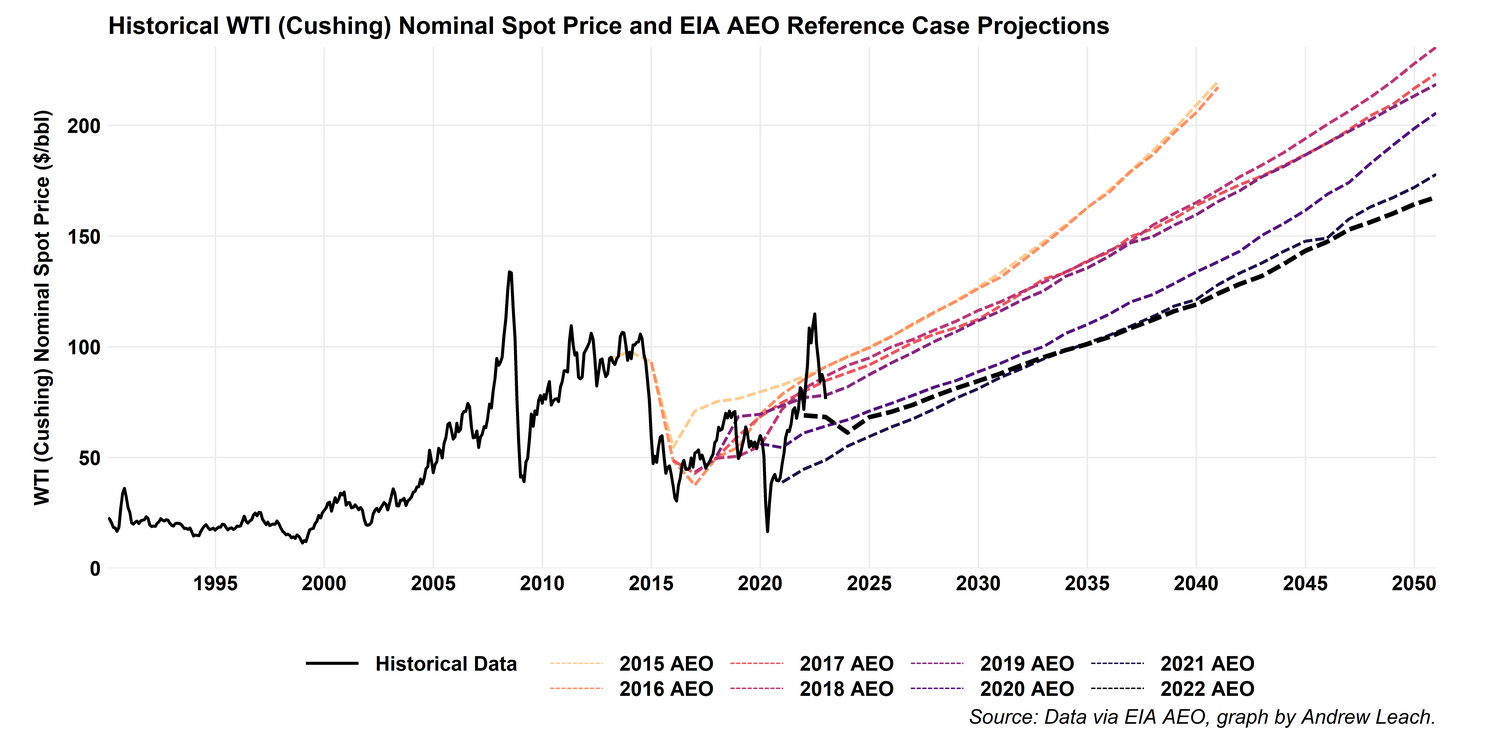

Yes, oil consumption continues to rise, but more slowly than previous increases and forecasts see demand increasing to much lower levels than would have been predicted just a few years ago.

And the gap between the January 2020 forecast and today’s forecast? That’s 1.2x Alberta’s production.

The story is much the same in the long run. And, despite recent price increases, the long run view on the value of oil is still tracking well below some of the older outlooks that underpinned major investments in oil production here in Alberta and elsewhere in the world.

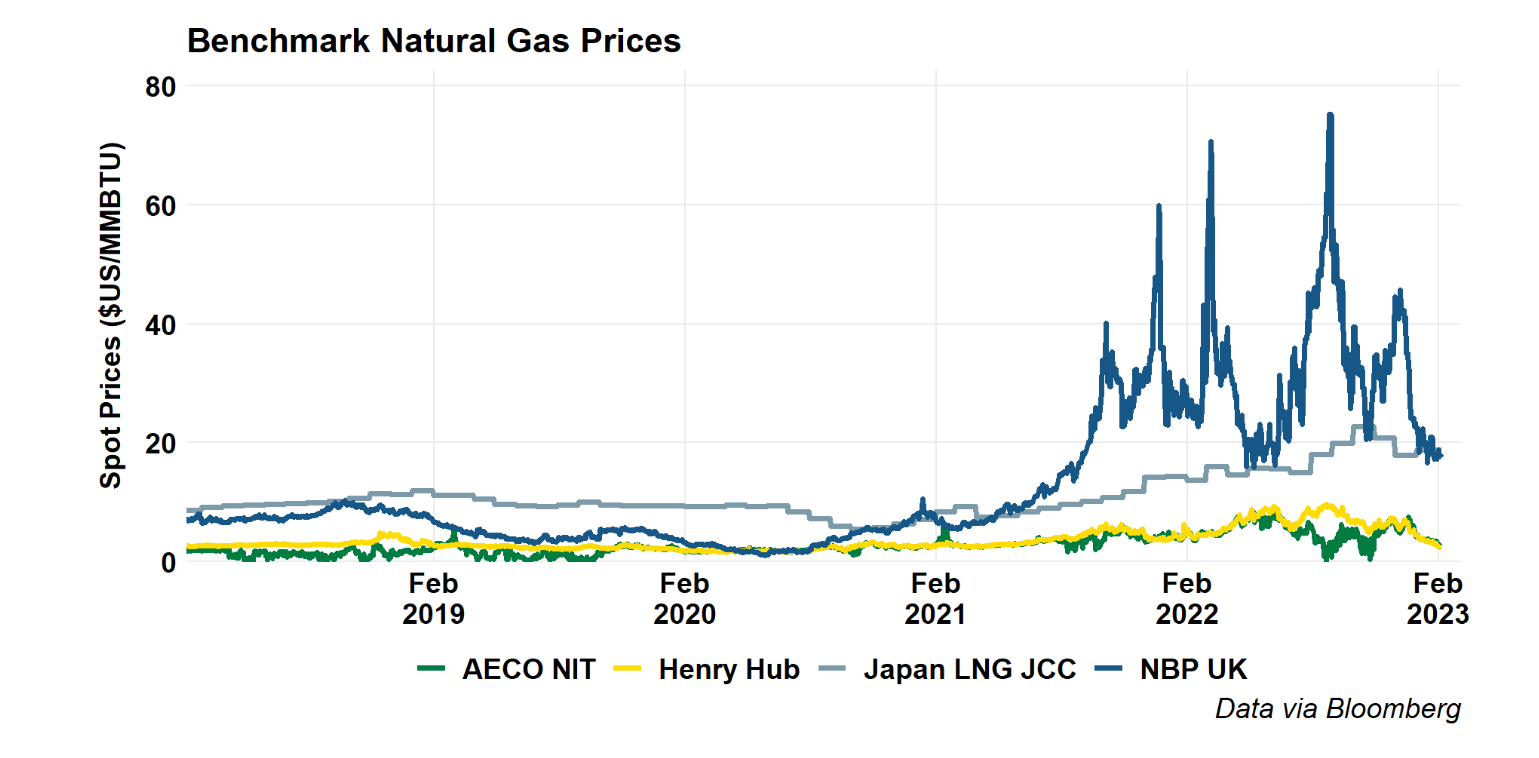

The last factor we’ll talk about tonight is the war in Ukraine, which has disrupted both oil and gas markets globally. The gas price spike in Europe has largely abated, thanks both to a warmer-than-expected winter and massive conservation efforts.

In Canada, this has led to renewed calls for the country to build LNG, increasing scrutiny on the Prime Minister’s comments regarding the business case for new terminals, and increased pressure on Ottawa and BC to relax climate change measures to permit and underpin new gas production and exports. Of course, not often present in those discussions is the reality that any new Canadian exports of natural gas are most of a decade away, and the world energy market will look substantially different by that time.

The business case for LNG conversation forces Canada (and the potential investors in any new plant) to wrestle not with the markets today, but what gas markets might look like in a world acting (or not acting) on climate change.

It’s going to force Canada to wrestle with its commitment to domestic targets, to domestic energy security, and to its allies.

There will be much talk of three-legged stools, I’m sure.

In the end, while the oil price shock of 2015 and the COVID crisis unquestionably took pressure off Canada in terms of policies to reduce emissions, the rebound in oil prices this year and, in particular, the war in Ukraine have put that pressure squarely back on. Canada has tough choices to make, as do many of its provinces.

I hope that we’ll see some of you tonight for more discussion of these issues.