Happy Friday. As usual, our charts and student stories are posted at https://aleach.ca/charts

In this week’s student stories, Youssaf Habib has a piece on this week’s fusion news, and deserves a shout out because he was the first person to bring the news to my attention. You can feel his excitement about it in the piece. Marc Vermette’s got a story on Vietnamese renewable funding to fill in some international news.

I’ve got six things for you this week.

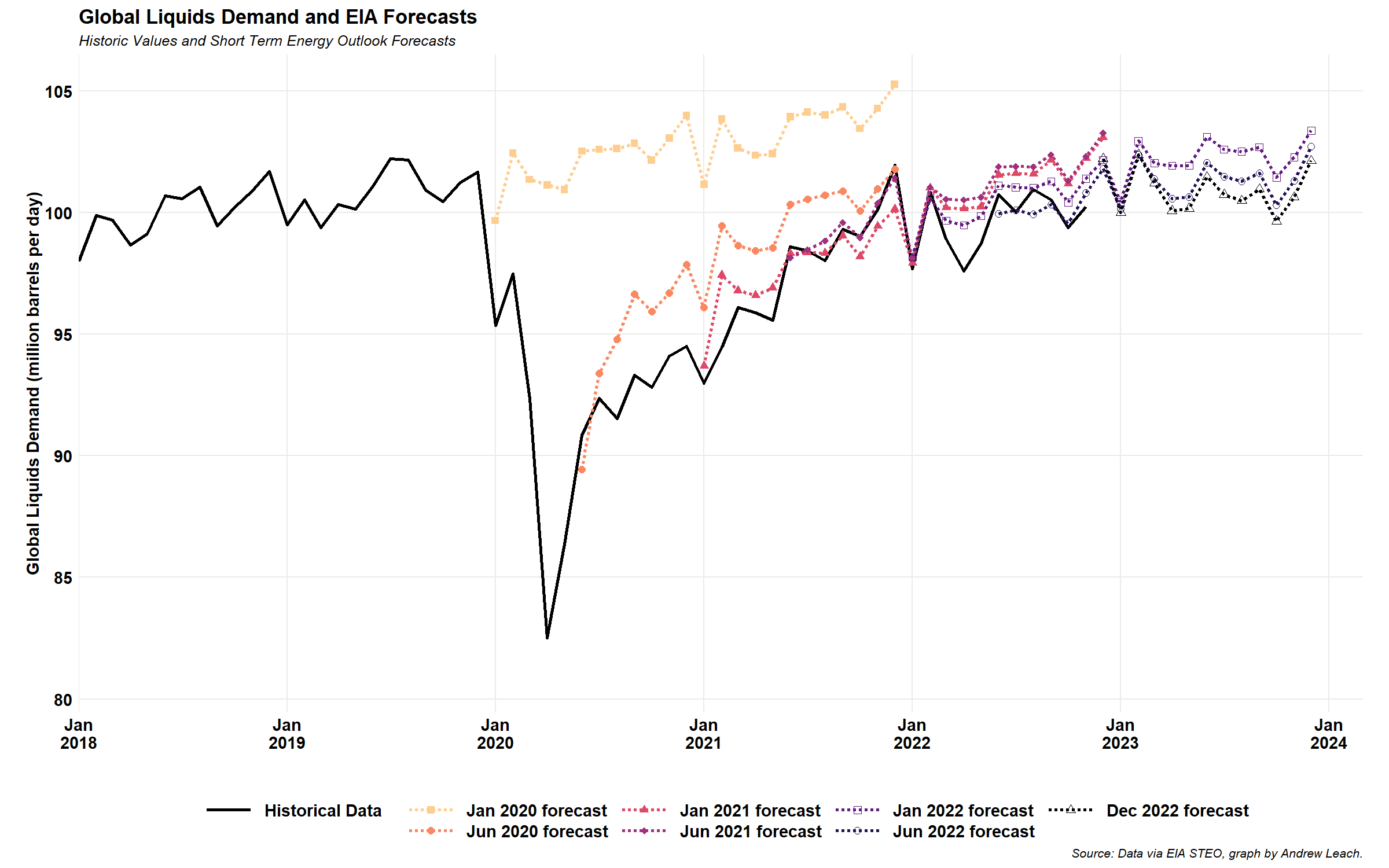

First off, I must make up for my missed EIA STEO update from last week.

My focus with the STEO continues to be the liquids demand outlook which, true to form, keeps trending downward, with consumption now not expected to get back to pre-COVID levels before late 2023. Pre-COVID, the EIA had forecast 105 million barrels per day of demand by the time last year. At it sits, we’re likely to be much closer to 100 million barrels per day than 105 million. A reminder that I keep a cache of a few STEO graphs updated here and you can access this and other similar data pages at my Projects page, although some I only update when specific classes are in session.

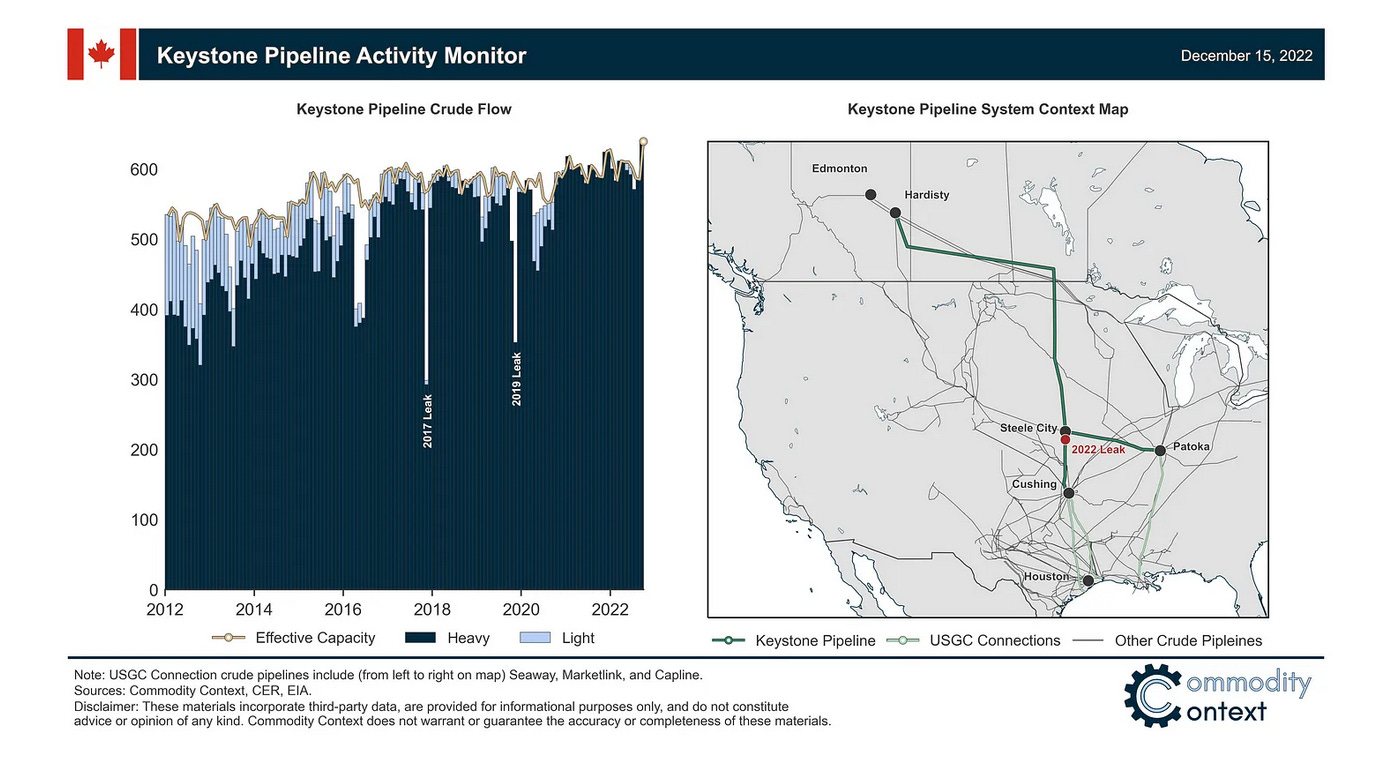

Still on the oil front, I should highlight another great piece from Rory Johnston at Commodity Context on the Keystone spill. As you can see from Rory’s slide below, the point of the spill, just downstream of the Wood River/Patoka lateral, means that this spill will have less immediate impact on the price of Canadian crude since, south of Steele City, there are other alternatives not available north of that point.

And, this afternoon, via Giovanni Staunovo, I learned that a specific Strategic Petroleum Reserve deal would help compensate for some of the barrels stranded by the spill.

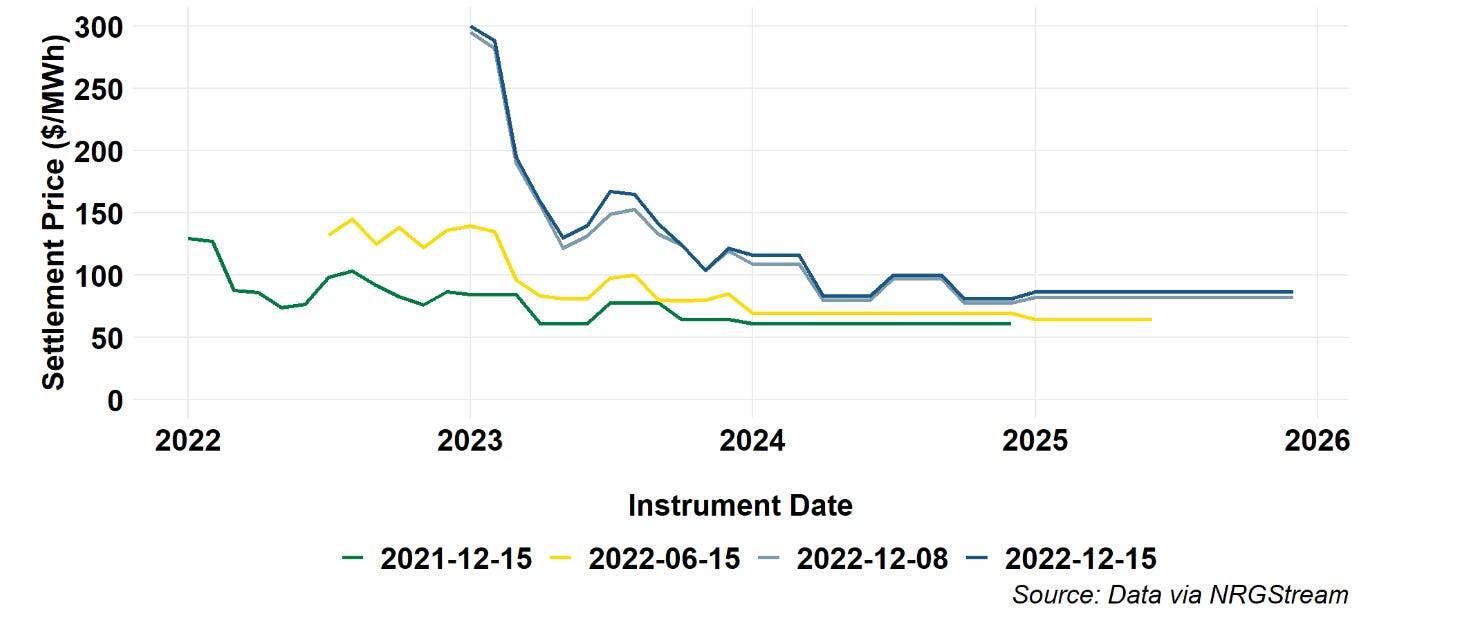

Closer to home, Calgary economist Blake Shaffer tweeted this image of Alberta power forwards, with a few comps that we don’t have in our weekly graph, so I thought it was worth sharing (and maybe also worth modifying ours).

The not at all a forecast of winter prices implied by the forward settlements just keeps getting worse for consumers (better for generators) for this winter and over the longer term as well as shown in our graph clipped below.

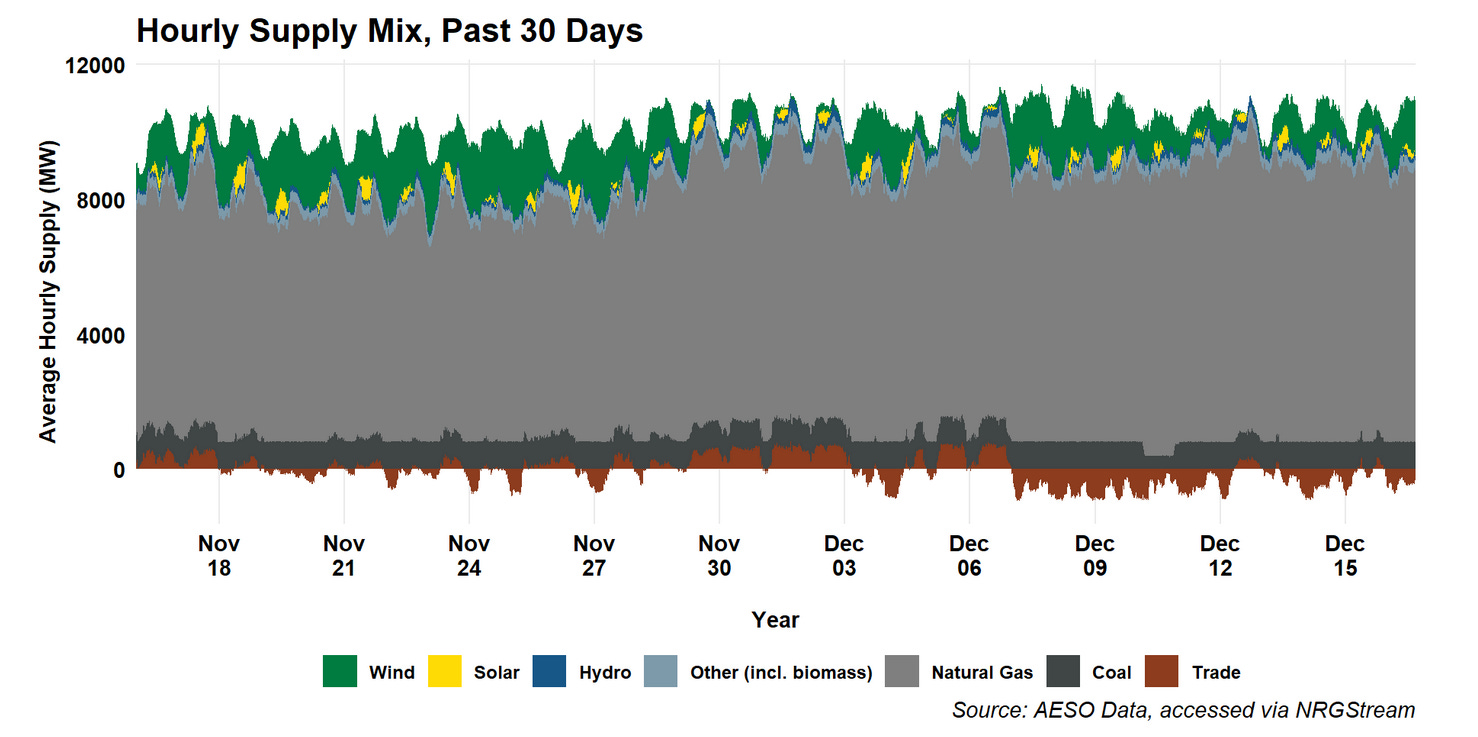

Also in the wholesale power market, we got really close to a coal-free hour this week, with a period with only one coal plant operating in the province. When will we see the first coal-free hour? My bet is sometime in late-April or early-May.

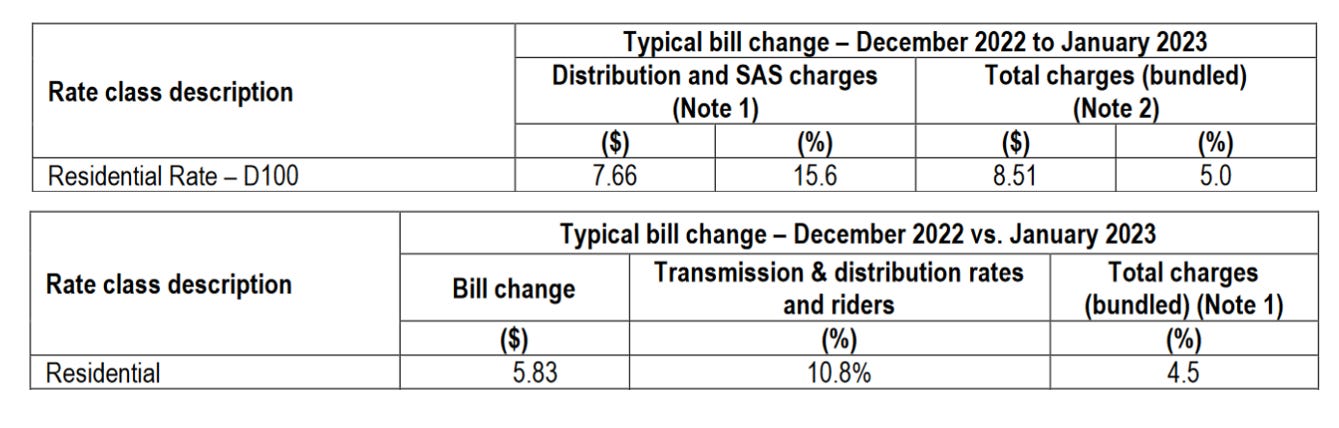

Next, as some of you will know, I’m teaching a utilities law class in the Faculty of Law this winter (yes, there are still seats!) and that’s led me to spend a lot of time in the bowels of the AUC eFiling system this week building a reading list. But, one thing you don’t have to go too far to see is the new rates for electricity distribution for 2023, and they’re not pretty. For a typical residential consumer, both EPCOR (10.8%) and ENMAX (15.6%) have been approved for large increases, while Fortis (6.2%) was approved today for a smaller increase.

Thanks to Blake Shaffer (again) and Jim Wachowicz for keeping me in the loop on these changes.

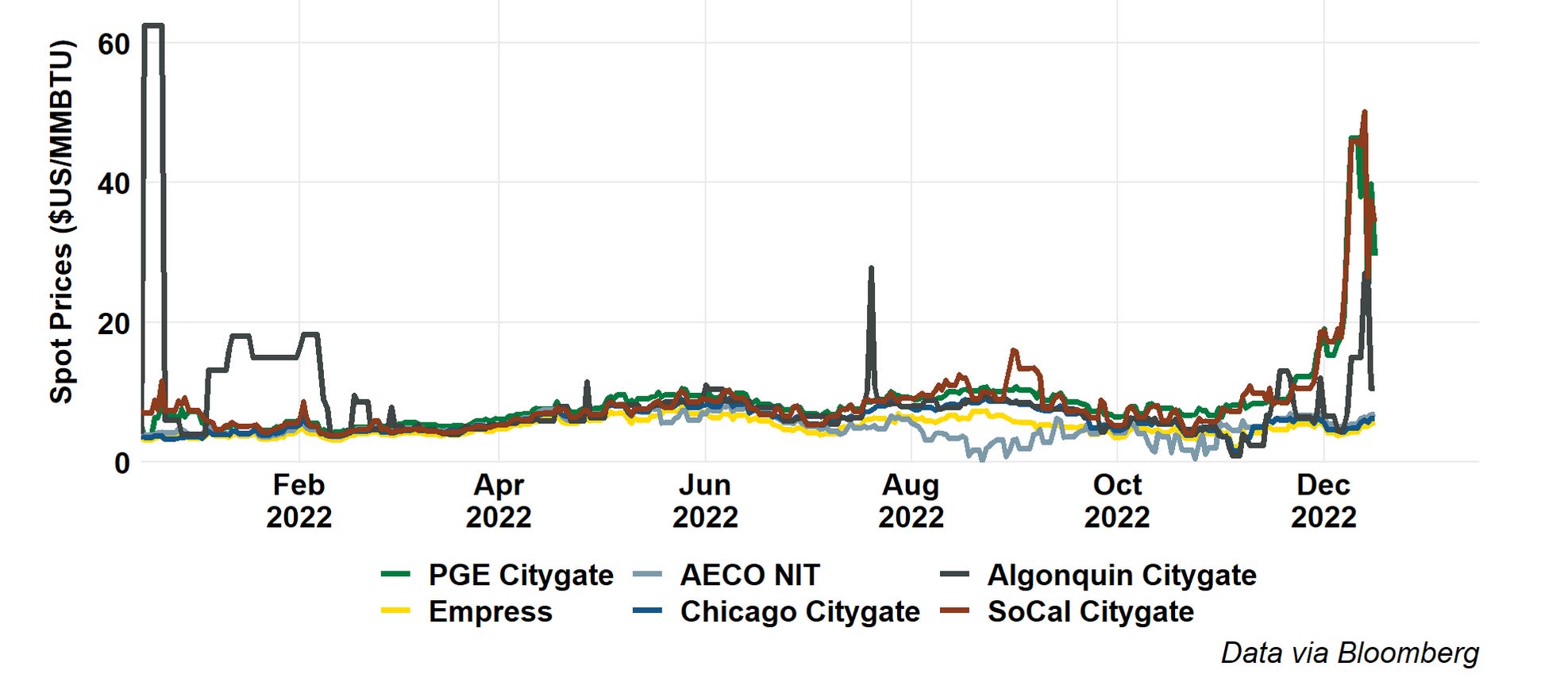

And, finally, make sure you take note of our North American gas hubs chart this week, with Algonquin (New England) joining the California hubs in pricing through the roof, although all three are down a bit at close yesterday. I’ve added SoCal Citygate pricing to our usual set this week, although the PG&E hub price captured the trend well before.

Have a great week. I’ll have some updates (likely story-free) over the break, and then we’ll be back to regular programming.